November 4, 2024

What's Behind the Numbers?

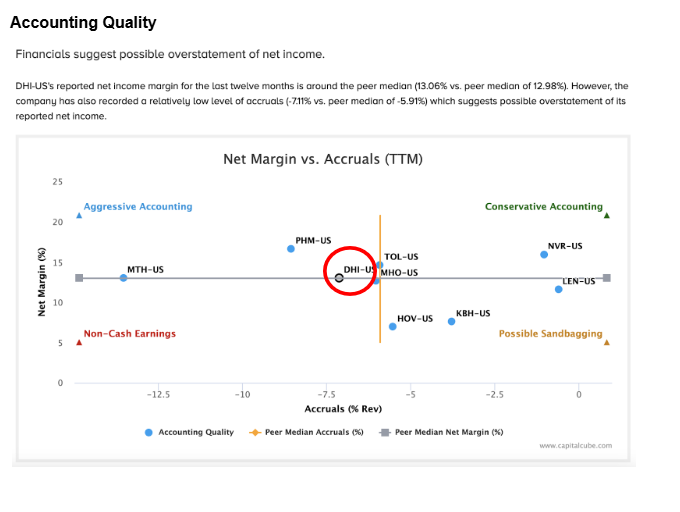

Last week, D.R. Horton (DHI-US), a leading homebuilder released third quarter earnings. To date, DHI appeared to be navigating the financial landscape of the past year with a seemingly steady hand. The company’s net income margin, standing at 13.06% for the last twelve months, is nearly identical to the peer average of 12.98%, hinting at stability and a solid bottom line. Yet, as we delve deeper, the story takes an intriguing turn.

Despite reporting healthy net income margins, DHI’s accruals tell a different story. Accruals, essentially management's estimates of non-cash expenses and liabilities, have taken a sharp dip to -7.11%, well below the peer median of -5.91%. In other words, DHI is not just using reserves, but draining them more aggressively than its competitors. This signals potential earnings management—leveraging reserves to elevate reported income, presenting a stronger facade of profitability than what might truly exist beneath the surface.

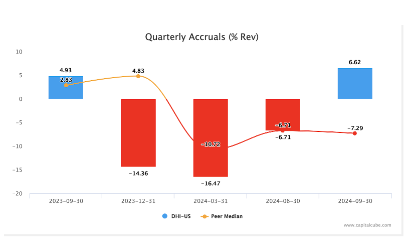

Rewind to 2023, DHI’s accruals-to-revenue ratio was -1.38%, but it has since slid to -7.11% over the trailing twelve months, diverging sharply from peers, whose median increased to -0.97%. The annual drop of 9.41 percentage points in DHI's accruals-to-revenue ratio underscores an unusually aggressive shift in reserve management. It’s like watching a tightrope walker lean forward to maintain balance—effective in the short run, but risky if pushed too far.

The quarterly performance paints a dramatic contrast. As of the latest quarter, DHI’s accruals-to-revenue ratio surged to 6.62% from -6.71% in March 2024, reaching its highest level in five quarters. Meanwhile, the peer median declined from -6.71% to -7.29%, marking a 13.91 percentage point leap for DHI relative to its peers. This spike raises questions: is DHI playing a strategic game, using reserves to bolster quarterly results, or are these shifts a sign of more systemic financial pressures?

DHI’s net income movements were largely driven by changes in Inventory, SG&A expenses, and Accounts Receivable. These categories, pivotal to operating cash flow, have significantly shaped DHI’s income story this year, excluding revenue changes. This focus on internal cost and asset management reflects the company’s efforts to maintain a positive narrative, even if it means aggressively managing reserves.

The broader implications for cash flow are clear: DHI's aggressive use of accruals may help paint a rosier earnings picture, but it also raises red flags about sustainability. If reserves continue to be used at this rate, the divergence between reported net income and actual cash flows could widen, affecting long-term operational health.

Ultimately, D.R. Horton’s financial narrative is one of impressive earnings management against the backdrop of an evolving housing market. It’s a story of resilience, but also one that prompts caution. As the company balances the line between accrual-based earnings and cash flow realities, investors should keep a close eye on how this strategic tightrope act unfolds in the coming quarters.

**All Images below are extracted from CapitalCube reports.

Earnings Quality

The company has been using up its reserves over the past year and it’s doing this at a faster rate than similar companies. Translation, it is spending more money than it's setting aside, which is a warning sign about its financial health.

For more information, register for a trial account on CapitalCube

Sign up for our mailing list today to receive news and updates - we won't spam you, we promise!